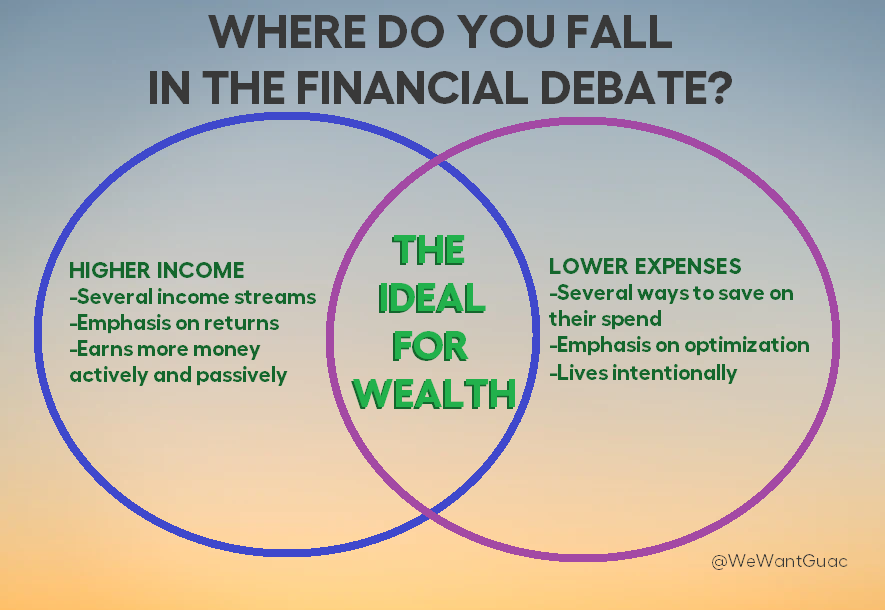

What’s Better, Greater Income or Lower Expenses?

You can tell which finance bloggers prefer which approach depending on their content. Some have built an audience with doing things like making your own cleaning products and building a simple, inexpensive lifestyle. Others go the other way, obsessing over dividends and all these side hustles they’ve got going on to stay on THE GRIND™.

Depending on your personality, one approach likely attracts you more than the other. Type As with endless energy and excitement will barrel into these higher-income forums. Type Bs who are more introverted homebodies will hang around discussions from the lower-expenses crowd.

I experience both sides of the coin – my large salary and investment streams give me a lot in common with the higher-income folks, but I also relate to the lower-expenses kids with my love for thrift shopping and getting most of my possessions for free. Because of that I make a good authority on which one is objectively better.

The Case for Higher Income

PROS

It is a hell of a lot easier to save money when you command a higher salary. A household making $50k a year will struggle much harder to save 50% than a household making $100k. In a very direct way, getting a larger paycheck makes building wealth a much more straightforward task. You don’t have to worry endlessly about your coffee runs or taxi rides hurting your savings aspirations. Why would you? Your investments already cover those expenses and then some!

CONS

Having a greater income won’t mean squat if you can’t control your spending. Thanks to a dearth of financial literacy in this country there’s a new class of workers called the high-earning poor. Sure, they have that high income so many others are envious of. Despite it, however, they still cannot improve their financial well-being.

It’s also not nearly as easy to reach these salary levels in the first place. By comparison, little habits that lower your spend are much more accessible to the common man.

The Case for Lower Expenses

PROS

Unlike earning a higher income, anyone can lower their expenses. I really do mean anyone. Both earning a higher salary and cutting your spend are hard to do, but the latter is easier than the former by far. Do you have to worry about more schooling, gaining more skillsets, and keeping up to date with the endless stream of economic news and how they’ll impact your livelihoods? No, who has the time?

All you have to do is get a little creative with what you do, like figuring out how to cook amazing meals at home or where you’ll get a nicer dining room table. Also? You feel like you have more control in your life this way – your success depends on YOUR efforts, not the mysterious movements of the stock market and supply/demand metrics.

CONS

There comes a point where you cannot lower your expenses any further, nor optimize the spending beyond what you’ve already have. It’s when you hit this point – where it really HURTS, it’s PAINFUL and even EMBARRASSING – that a higher income is your only choice if you want to save any more money. That’s a bitter pill to swallow if you’re already overwhelmed by how you break into those higher-paying titles.

My Solution

I straddle the line that separates these two camps. Nobody’s trying to force me to one side or the other (yet) but even if they did I’d stay on that line. That’s the only place where your low expenses aren’t strained and your higher income brings more money in than it leaks out. Both approaches are necessary. They go hand-in-hand to have you build true, sustainable wealth.

You cannot approach personal finance with the question “Should I aim for higher income or for lower expenses?” Either way you’re not going to have a peaceful way to wealth. Instead, your question has to be “Should I aim FIRST for higher income or for lower expenses?” That FIRST is the key word in your hypothetical question, which depends specifically on your life circumstances. If you’re a college student with loans to pay or a parent worried about how you’ll afford childcare, trying to focus on both approaches will give you nothing but stress and shame.

Same goes for if you’re struggling to understand why you’re never left with money at the end of the month, despite having a decent wage. Be honest with yourself that BOTH approaches are necessary, and then give yourself ONE of them to conquer first. This helps you so much by simplifying your goals, and you’re much more likely to hit you goal if you keep it to one.

What do you think? Is this approach the right one or am I missing something major we need to consider?